Income Capitalization

![]()

Income Capitalization

The new income approach is a 2-page set:

- Page 1: Capitalization rate documentation from sales in the competitive market area with similar land composition,

- Page 2: Subject's income and expense estimates with final net income computation and conversion to a value estimate with the market capitalization rate selected.

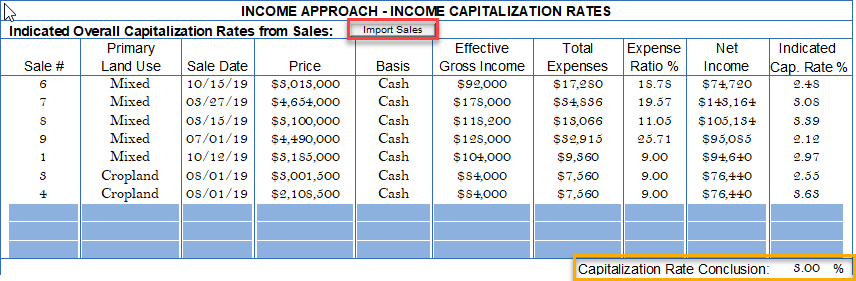

The sale’s capitalization rates (cap rates) are pulled into the grid via the “Import Sales” button shown in red.

As explained in the ASFMRA’s textbooks, property composition, expense ratios, size, dates, and rates are used in the final capitalization rate selection at 3% for this example.

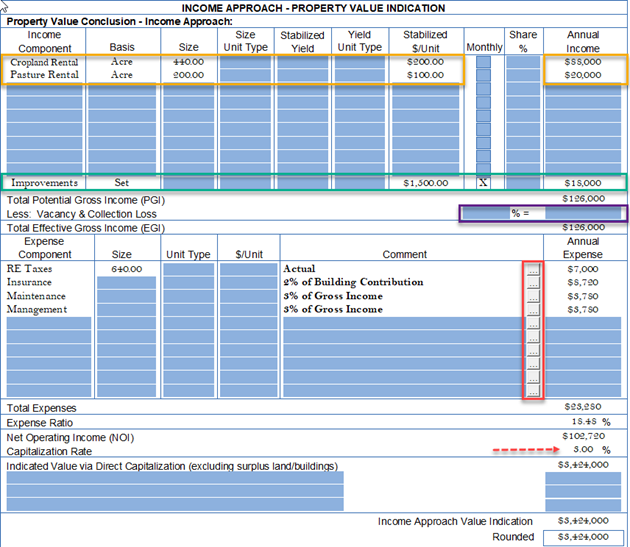

The subject’s value is provided on the next grid.

This income form design is slightly different than the “original” income approach in the former “Forms Library”. There are no check boxes for “cash”, “share”, or “owner/operator” income. ClickForms assumes if the “Share %” is entered, income is computed on that basis. Owner/operator income is nearly impossible to obtain on comparable sales; thus, it is assumed to be “cash” when the “Stabilized $/Unit” is entered. If owner/operator income is applied, include that basis in the “Income Comments” on the “Income Capitalization Rates” form shown on the prior page.

Some clients require “vacancy & collection loss” percentages or VCL (purple) to be added. This is typical for urban properties, but rarely for rural types --- unless they are building intensive (facilities). Practically, whether its included or not, make sure the sales are analyzed like the subject. The result is, if VCL is included, net income declines and the cap rate is smaller. If VCL is excluded like this example, the net income increases, and the cap rate increases. As long as the procedure is the same as the subject, the impact of VCL is built into the resulting cap rate and automatically reflected in the result.

The red boxes on each expense line launches a calculator. The user can enter a percentage and select one of six (6) components for multiplication of the expense (shown on prior example). The real estate taxes are actual; thus, no calculation. However, the three (3) remaining expenses can be calculated with the tool as follows:

- Insurance = 2% of Improvement Contribution (selected from pull-down list)

- Maintenance = 3% of Gross Income (selected from pull-down list)

- Maintenance = 3% of Gross Income (selected from pull-down list) --- Note: this is passive management not active or “hands on” full time.

The final 3% cap rate (red arrow) is applied from the first form in this 2-page set.